A special purpose entity is a legally independent company that is established to implement a clearly defined economic project. Internationally, special purpose vehicles are often referred to as special purpose entities (SPEs) or special purpose vehicles (SPVs). Despite the different names, they pursue the same purpose: the implementation of a clearly defined, isolated economic project.

In recent years, the use of special purpose vehicles (SPVs) has increased significantly, particularly in the venture capital market. According to Carta, the number of new SPVs increased significantly during the VC boom in 2021. Although the pace has slowed since then, the long-term trend is clearly upward.

But SPVs are not only used in venture capital. They are also a key instrument for structuring complex projects in many other economic sectors.

What Is a Special Purpose Entity?

A special purpose entity is a legally independent company with a defined purpose. It is often established to isolate certain assets, projects, or financing. The purpose of the separation is to limit risks, shift liability, or optimize financing structures.

The choice of legal form depends heavily on the location and the economic objective:

In many cases, special purpose entities are created for projects, real estate, infrastructure, or financing arrangements. A clear allocation facilitates control, transparency, and risk management within the group.

What Does SPE/SPV Mean?

The terms SPE and SPV originate from international accounting and financial practice.

- Special Purpose Entity (SPE) refers to a company that is established for a specific economic purpose.

- Special Purpose Vehicle (SPV) essentially describes the same concept, but is often used in connection with financing, securitization, or project companies.

Both terms are often used interchangeably in the international environment. In practice, the use often depends on the context or the respective accounting standard.

How Is a Special Purpose Entity Structured?

The structure of a special purpose entity is usually deliberately simple and functional. The aim is to present the legal and economic separation from the parent company as clearly as possible.

Typical characteristics of a special purpose entity are:

This structure enables a clear separation between the project within the special purpose entity and the rest of the group.

Why Are Special Purpose Entities Established?

Companies set up special purpose entities primarily to clearly separate risks, assets, and financing from the core business. This structure allows individual projects to be organized and managed in isolation.

A key advantage is the limitation of risk for the parent company, as financial obligations are often limited to the special purpose entity. At the same time, such a structure facilitates the implementation of complex financing, for example for large infrastructure or real estate projects.

Special purpose entities are also used to optimize accounting or tax treatment and to involve external investors in individual projects without them having a direct stake in the company as a whole.

Typical Use Cases

Special purpose entities help companies to limit risks and separate individual projects legally and financially from the rest of the company. Typical areas of application are:

Advantages and Disadvantages of Special Purpose Vehicles

Special purpose entities offer companies various strategic and financial advantages, but also entail additional organizational and regulatory challenges:

| ADVANTAGES | DISADVANTAGES |

|---|---|

| Risk separation: Financial risks are usually limited to the special purpose vehicle. | More complex structure: Additional entities increase the administrative burden. |

| Transparent project structure: Projects can be analyzed more clearly in economic terms. | Regulatory requirements: Additional reporting and documentation requirements. |

| Flexible financing: Equity and debt can be structured on a project-specific basis. | Consolidation obligation: Special purpose entities must often be included in the consolidated financial statements. |

When Is There an Obligation to Consolidate?

Whether a special purpose entity must be included in the consolidated financial statements depends on the respective accounting regulations.

The decisive factor is generally the question of who exercises economic control over the company. A consolidation obligation can arise if a company:

Both international standards and national accounting regulations are increasingly taking the economic content of the structure into account.

What Is a Special Purpose Entity in the HGB Group?

Under German commercial law, a special purpose entity can be part of a group if the parent company exercises a controlling influence. It is not only the legal structure that is decisive here, but above all the actual economic control.

Formally independent companies can therefore also be considered subsidiaries and may have to be included in the consolidated financial statements in accordance with the German Commercial Code (HGB). Participation structures, contractual control rights and economic dependencies are particularly important in this regard.

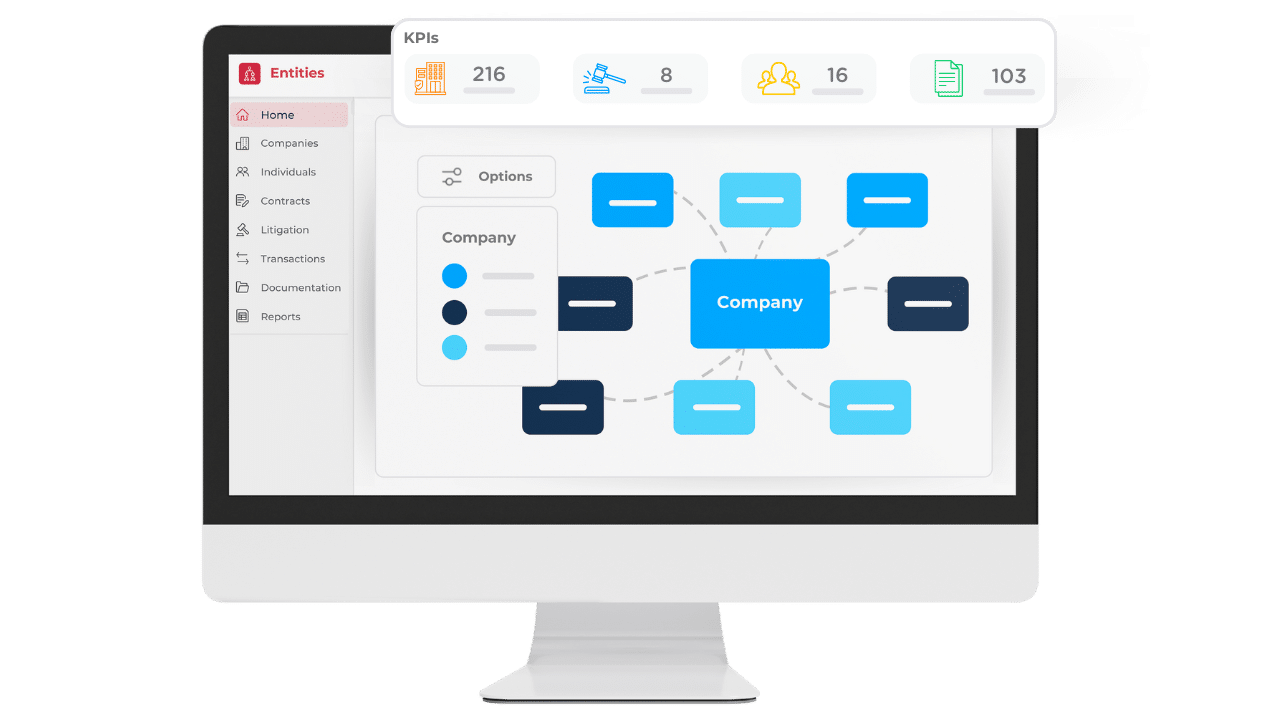

How Entity Management Helps with SPE/SPV

The management of special purpose entities such as SPEs or SPVs can be complex, as numerous companies, investments and contracts need to be managed. Efficient entity management ensures transparency, clear structures and a central overview of all relevant data. This allows risks to be reduced, compliance requirements to be met and administrative expenses to be significantly lowered.

With DiliTrust’s entity management, companies can centrally manage company data, shareholdings, powers of attorney and documents. Changes are automatically documented, shareholding structures can be clearly visualized, and deadlines and compliance obligations are reliably monitored. DiliTrust thus enables efficient, transparent and secure management of SPEs and SPVs.

Discover your savings

Calculate your potential annual benefit by streamlining governance and centralizing corporate records with DiliTrust.